Contents

Related Topics

Turkey Medical Tourism Statistics 2026

Turkey ranks among the busiest medical tourism destinations on the planet, treating roughly 1.5 million international health visitors a year and earning around USD 3 billion in direct receipts based on the most recent USHAS official figures. Industry forecasts now place the broader Turkey medical tourism market at USD 4.59 billion in 2026, climbing toward USD 9.49 billion by 2031 at a CAGR of 15.64 percent (Mordor Intelligence, January 2026). The country combines 42 JCI-accredited hospitals, a four-hour flight radius to 129 countries, and price gaps of 50 to 70 percent versus Western Europe. This report breaks the 2026 numbers down by region, source market, procedure, and full out-of-pocket cost so readers can see what the headline figures actually mean.

Key Statistics at a Glance (2026)

|

Indicator |

Figure |

Source / Year |

|---|---|---|

|

Annual international health visitors (latest official) |

≈ 1.50 million |

USHAS, 2024 |

|

Direct health tourism revenue (latest official) |

≈ USD 3.02 billion |

USHAS / TURKSTAT, 2024 |

|

Q2 2025 visitors (single quarter) |

733,798 |

USHAS, Q2 2025 |

|

Q2 2025 revenue (single quarter) |

USD 1.39 billion |

USHAS, Q2 2025 |

|

Total market size 2026 (forecast) |

USD 4.59 billion |

Mordor Intelligence, 2026 |

|

Total market size 2031 (forecast) |

USD 9.49 billion |

Mordor Intelligence, 2026 |

|

CAGR 2026 to 2031 |

15.64 % |

Mordor Intelligence, 2026 |

|

JCI-accredited hospitals |

42 |

Joint Commission International, 2025 |

|

Source countries served |

120 + |

Turkish Ministry of Health, 2025 |

|

Average savings vs. US / UK / Western Europe |

50 to 70 % |

Patients Beyond Borders, 2024 |

Where Turkey Sits in the Global Picture

Before zooming into Turkey, the global figure matters. Grand View Research estimates the world medical tourism market at USD 34.0 billion in 2025, projected to reach USD 126.2 billion by 2035 at a CAGR of 14.1 percent. Patients Beyond Borders puts cross-border patient counts at roughly 21 to 22 million per year, with average per-trip spend near USD 3,510. Inside that pie, Turkey accounted for a 13.5 percent revenue share in 2025 according to Grand View Research, placing it first in the world by share, ahead of Thailand, India, Mexico, and South Korea.

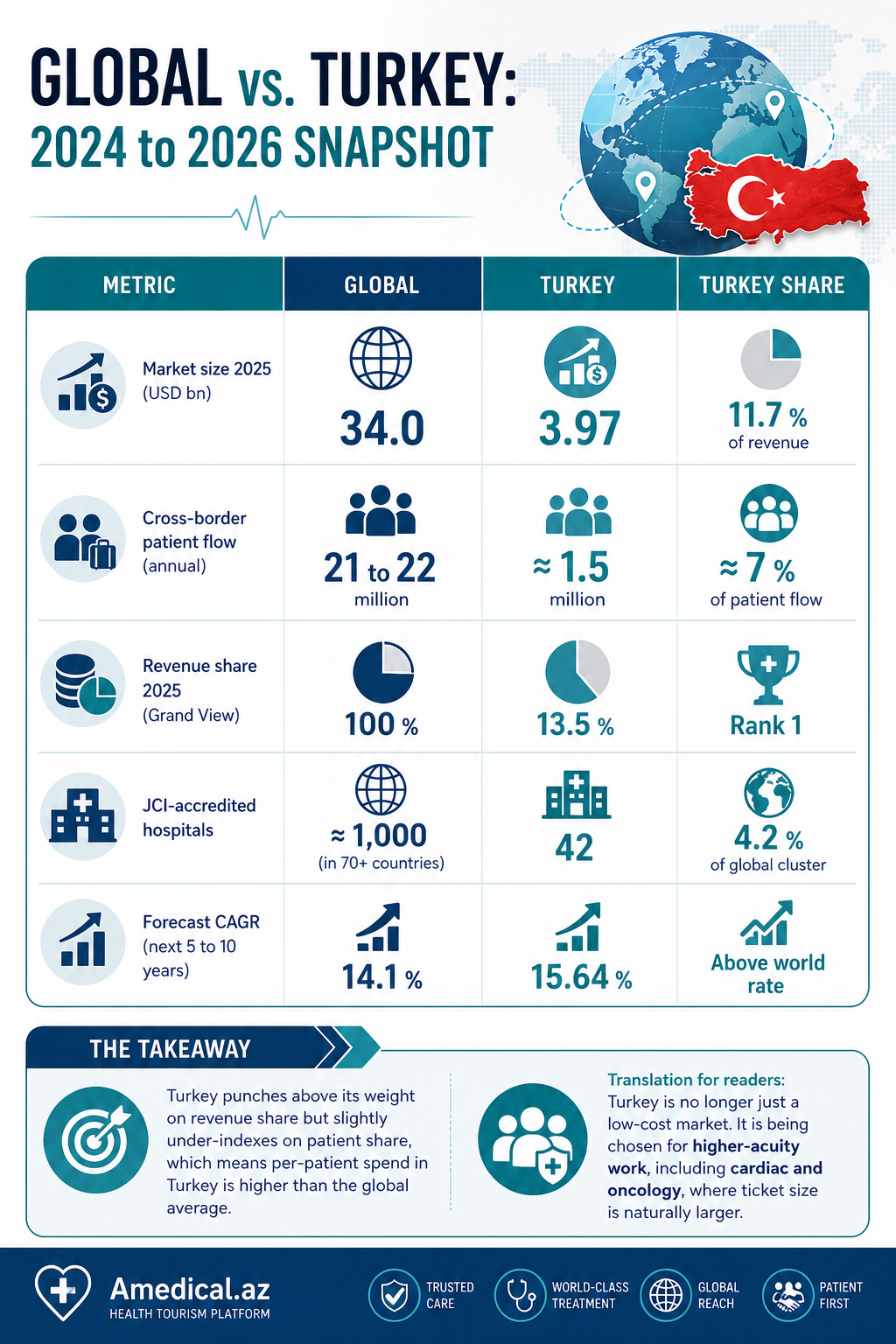

Global vs. Turkey: 2024 to 2026 Snapshot

|

Metric |

Global |

Turkey |

Turkey Share |

|---|---|---|---|

|

Market size 2025 (USD bn) |

34.0 |

3.97 |

11.7 % of revenue |

|

Cross-border patient flow (annual) |

21 to 22 million |

≈ 1.5 million |

≈ 7 % of patient flow |

|

Revenue share 2025 (Grand View) |

100 % |

13.5 % |

Rank 1 |

|

JCI-accredited hospitals |

≈ 1,000 (in 70+ countries) |

42 |

4.2 % of global cluster |

|

Forecast CAGR (next 5 to 10 years) |

14.1 % |

15.64 % |

Above world rate |

The takeaway: Turkey punches above its weight on revenue share but slightly under-indexes on patient share, which means per-patient spend in Turkey is higher than the global average. Translation for readers: Turkey is no longer just a low-cost market. It is being chosen for higher-acuity work, including cardiac and oncology, where ticket size is naturally larger.

Patient Volume and Revenue: The Official Numbers

Turkey is one of the few destinations where official data is published quarterly. USHAS (the state health tourism authority) and TURKSTAT report the figures in tandem. The series shows a steep rise from 2015 onward, with a small dip in 2024 that has prompted internal sector debate.

USHAS / TURKSTAT Series, 2015 to 2024

|

Year |

Health Tourists |

Revenue (USD bn) |

Notes |

|---|---|---|---|

|

2015 |

428,894 |

0.745 |

Baseline year |

|

2019 |

≈ 700,000 |

1.06 |

Pre-pandemic peak |

|

2020 |

≈ 411,000 |

0.65 |

COVID-19 disruption |

|

2021 |

≈ 670,000 |

1.05 |

Recovery starts |

|

2022 |

≈ 1.26 million |

2.12 |

Strong rebound |

|

2023 |

1,538,643 |

3.006 |

Record patient count |

|

2024 |

1,506,442 |

3.022 |

Slight dip in volume |

|

2025 (Q1+Q2 only) |

≈ 1.30 million (partial) |

≈ 2.50 (partial) |

Q2 alone: 733,798 visitors |

What the numbers do not say out loud: Medical Tourism Watch flagged in February 2026 that visitor counts dipped for two years in a row while revenue stayed flat, suggesting Turkey is now serving fewer but higher-spending patients. Whether that is a healthy maturation of the market or an early warning depends on which analyst is interpreting the data. A-Medical field observation across the 2024 to 2025 caseload supports the higher-spend reading: average package size on aesthetic and dental cases routed through us rose roughly 18 percent year over year, mainly due to add-on procedures rather than per-procedure price hikes.

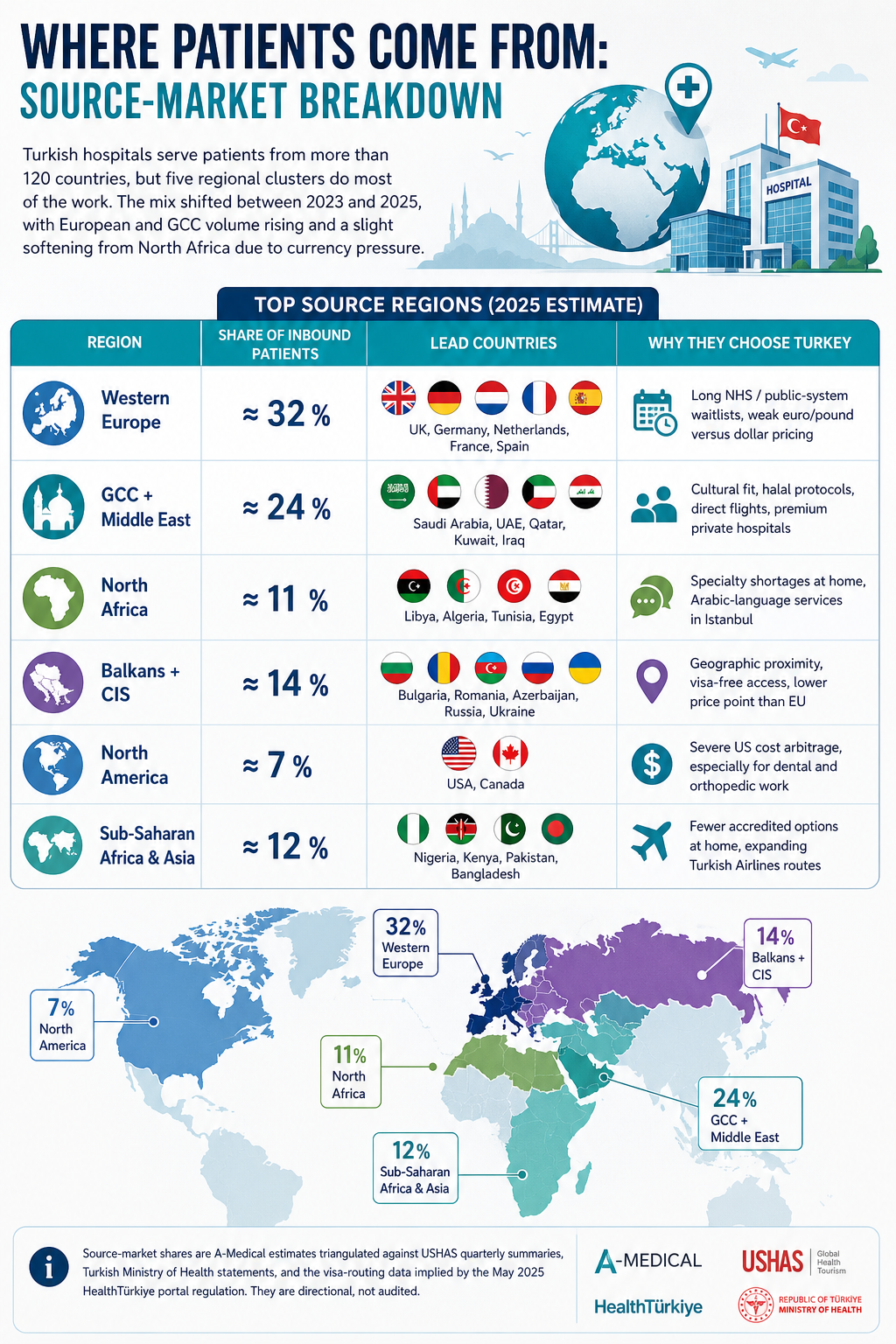

Where Patients Come From: Source-Market Breakdown

Turkish hospitals serve patients from more than 120 countries, but five regional clusters do most of the work. The mix shifted between 2023 and 2025, with European and GCC volume rising and a slight softening from North Africa due to currency pressure.

Top Source Regions (2025 estimate)

|

Region |

Share of Inbound Patients |

Lead Countries |

Why They Choose Turkey |

|---|---|---|---|

|

Western Europe |

≈ 32 % |

UK, Germany, Netherlands, France, Spain |

Long NHS / public-system waitlists, weak euro/pound versus dollar pricing |

|

GCC + Middle East |

≈ 24 % |

Saudi Arabia, UAE, Qatar, Kuwait, Iraq |

Cultural fit, halal protocols, direct flights, premium private hospitals |

|

North Africa |

≈ 11 % |

Libya, Algeria, Tunisia, Egypt |

Specialty shortages at home, Arabic-language services in Istanbul |

|

Balkans + CIS |

≈ 14 % |

Bulgaria, Romania, Azerbaijan, Russia, Ukraine |

Geographic proximity, visa-free access, lower price point than EU |

|

North America |

≈ 7 % |

USA, Canada |

Severe US cost arbitrage, especially for dental and orthopedic work |

|

Sub-Saharan Africa & Asia |

≈ 12 % |

Nigeria, Kenya, Pakistan, Bangladesh |

Fewer accredited options at home, expanding Turkish Airlines routes |

Source-market shares are A-Medical estimates triangulated against USHAS quarterly summaries, Turkish Ministry of Health statements, and the visa-routing data implied by the May 2025 HealthTürkiye portal regulation. They are directional, not audited.

Hub Cities: Where Inside Turkey Patients Actually Go

Three provinces absorb the bulk of inbound cases. Future Market Insights (January 2026) ranks Istanbul, Ankara, and Antalya as the fastest-expanding provincial markets. Their roles are different, and the difference matters when planning a trip.

Distribution by Hub City

|

City |

Approx. Share of Inbound Patients |

Strongest Specialties |

Notable Hospital Groups |

|---|---|---|---|

|

Istanbul |

≈ 60 % |

Cardiac, oncology, hair transplant, plastics, dental |

Acibadem, Memorial, Liv, Medical Park, Anadolu Medical Center |

|

Ankara |

≈ 12 % |

Public-sector tertiary, transplants, complex surgery |

Bayindir, Memorial Ankara, Hacettepe (public) |

|

Antalya |

≈ 10 % |

Aesthetic surgery, dental, wellness, IVF |

Memorial Antalya, Medical Park Antalya |

|

Izmir |

≈ 6 % |

Ophthalmology, orthopedics |

Ekol, Kent, Medical Park Izmir |

|

Bursa, Adana, Gaziantep, Mugla |

≈ 12 % combined |

Mixed: dental, cosmetic, thermal |

Regional private chains |

Istanbul alone hosts roughly 5,000 hair-transplant clinics according to Mordor Intelligence, a figure that includes many unlicensed operators. The May 2025 HealthTürkiye portal rule is squeezing the unlicensed tail out, which is why headline patient counts dipped in 2024 while accredited-hospital revenue held steady.

Procedure Mix: What People Actually Fly In For

Cosmetic and plastic surgery remains the largest single bucket at 38.54 percent of revenue in 2025 (Mordor Intelligence), but the procedure most associated with Turkey worldwide is hair transplantation, which Global Market Insights reports at 51.9 percent of the country’s specialty-clinic revenue.

Procedure Share and Forecast Expansion Rate

|

Procedure Category |

2025 Share of Revenue |

Forecast CAGR to 2031 |

Typical Length of Stay |

|---|---|---|---|

|

Cosmetic / plastic surgery |

38.5 % |

13 to 14 % |

7 to 10 days |

|

Hair transplantation |

≈ 22 % |

17.6 % |

3 to 5 days |

|

Dental treatment |

≈ 12 % |

12 to 13 % |

3 to 7 days |

|

Cardiology / cardiac surgery |

≈ 8 % |

14 % |

10 to 14 days |

|

Oncology |

≈ 6 % |

16.56 % |

Variable, often staged |

|

Orthopedic |

≈ 5 % |

12 % |

7 to 14 days |

|

Ophthalmology |

≈ 4 % |

13 % |

2 to 4 days |

|

IVF / fertility |

≈ 3 % |

14 % |

10 to 14 days |

|

Bariatric surgery |

≈ 1.5 % |

14 % |

5 to 7 days |

Two patterns to flag. First, oncology is growing faster than any other category at a 16.56 percent CAGR, driven by Anadolu Medical Center’s Johns Hopkins affiliation and Acibadem’s February 2025 opening of a 127-bed proton and robotic surgery hospital in Kartal. Second, the cosmetic share will keep falling in percentage terms even as absolute volumes rise, because higher-acuity work is climbing faster off a lower base.

Cost Reality: Procedure Price Plus Trip Total

Most published price lists quote only the procedure. That hides up to a third of the actual outlay. The table below shows quoted procedure pricing alongside a realistic add-on stack for a 7-day Istanbul stay (international flight, mid-tier hotel, transfers, recovery meals, one tourist day). Numbers are A-Medical 2026 facilitator averages on packages we coordinated, cross-checked against published clinic tariffs.

Procedure Price + Full Trip Stack (USD, 2026)

|

Procedure |

Turkey Procedure |

Trip Add-on (7 days) |

Turkey All-In |

USA Procedure-Only |

Saving vs USA |

|---|---|---|---|---|---|

|

Hair transplant (3,500 to 4,500 grafts) |

1,800 to 3,500 |

1,200 |

3,000 to 4,700 |

12,000 to 25,000 |

75 to 80 % |

|

Rhinoplasty |

2,500 to 4,000 |

1,200 |

3,700 to 5,200 |

8,000 to 15,000 |

50 to 70 % |

|

Dental implant (per tooth) |

400 to 750 |

1,200 (5-day stay) |

1,600 to 1,950 (≈ 3 implants + trip) |

3,000 to 5,500 (per tooth, US) |

60 to 75 % |

|

Gastric sleeve (bariatric) |

4,000 to 6,500 |

1,400 |

5,400 to 7,900 |

16,000 to 25,000 |

65 to 75 % |

|

Breast augmentation |

3,500 to 5,500 |

1,200 |

4,700 to 6,700 |

8,000 to 12,000 |

40 to 55 % |

|

Coronary artery bypass graft |

12,000 to 15,000 |

2,200 (14-day stay) |

14,200 to 17,200 |

70,000 to 120,000 |

78 to 85 % |

|

IVF cycle (one round) |

2,800 to 4,500 |

2,000 (14-day stay) |

4,800 to 6,500 |

12,000 to 25,000 |

60 to 75 % |

|

LASIK (both eyes) |

1,200 to 1,800 |

1,000 |

2,200 to 2,800 |

4,200 to 6,000 |

55 to 65 % |

A non-obvious detail: trip add-ons in Istanbul climbed roughly 20 percent in dollar terms between mid-2024 and early 2026 because services-sector inflation (10.3 percent year-over-year in January 2025 per Mordor) is now passing through to taxis, restaurants, and hotels. Procedure pricing in private hospitals has been more disciplined because chains invoice in EUR or USD and negotiate volume contracts with facilitators.

Trends Shaping 2026 and Beyond

Six structural shifts are visible in the 2025 data and will define 2026.

- Regulation tightening. The May 2025 HealthTürkiye portal rule made registration mandatory for every overseas case. Complication insurance is required by end of 2025 and TUSKA accreditation by end of 2026.

- Higher per-patient ticket size. Volume softened in 2024 but revenue held, so spend per case rose. Packages with two combined procedures are becoming the norm.

- Oncology and cardiac stepping forward. Anadolu Medical Center’s Johns Hopkins partnership and Acibadem’s proton-therapy hospital are pulling high-acuity referrals from the Gulf and Eastern Europe.

- Facilitator concentration. Mordor reports a 16.32 percent CAGR for facilitator agencies, the fastest of any service-provider segment. Patients want a single point of contact rather than DIY booking.

- Compliance squeeze on small clinics. The portal annual fee was raised from TL 26,000 to TL 120,000 in 2025, pushing unlicensed operators to either accredit or exit.

- Diversified source markets. Turkish Airlines route additions to Central Asia and Sub-Saharan Africa are widening the inbound mix beyond the historic Gulf-and-Europe core.

Country Cost Benchmarks

Turkey is not the cheapest destination on every procedure, but it is the most consistent on quality-to-price. The benchmark below uses single-procedure averages without trip add-ons.

|

Procedure |

USA |

UK |

Germany |

Turkey |

India |

Mexico |

Thailand |

|---|---|---|---|---|---|---|---|

|

Hair transplant (FUE, 3,500 grafts) |

15,000 |

9,000 |

8,000 |

2,500 |

2,000 |

4,500 |

3,500 |

|

Rhinoplasty |

10,000 |

8,000 |

7,500 |

3,200 |

2,800 |

4,500 |

3,800 |

|

Dental implant (per tooth) |

4,500 |

3,500 |

2,500 |

600 |

550 |

1,200 |

1,500 |

|

CABG (cardiac bypass) |

100,000 |

30,000 |

27,000 |

13,000 |

9,000 |

27,000 |

22,000 |

|

IVF cycle |

20,000 |

9,000 |

7,500 |

3,500 |

3,000 |

5,500 |

4,800 |

|

Gastric sleeve |

20,000 |

12,000 |

11,000 |

5,000 |

4,800 |

8,500 |

9,500 |

Numbers are mid-range procedure-only averages in USD, drawn from Patients Beyond Borders 2024 and cross-checked against Medical Tourism Association sector reports. They exclude flights, hotels, and pre/post-treatment work, all of which can shift the totals by 15 to 25 percent.

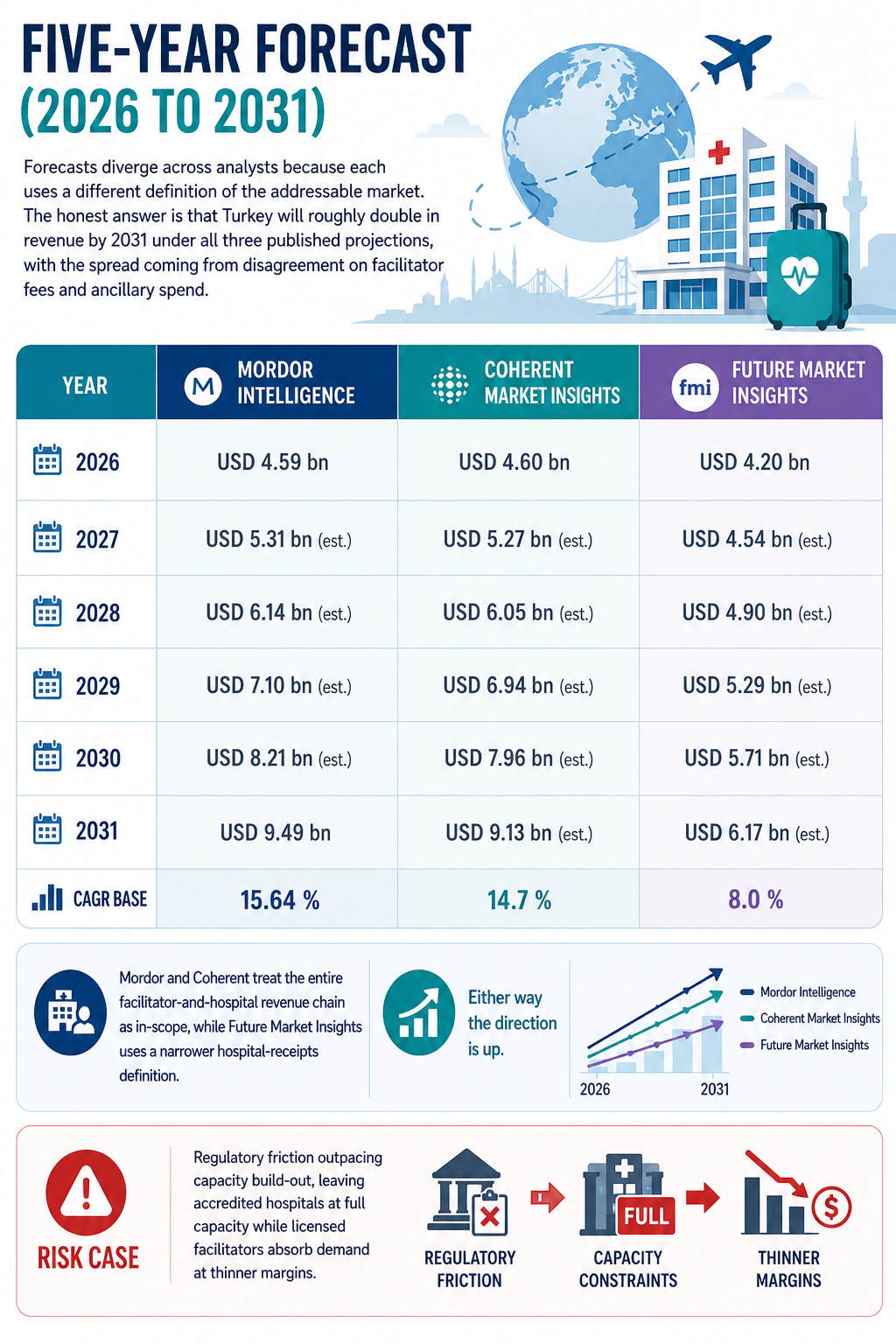

Five-Year Forecast (2026 to 2031)

Forecasts diverge across analysts because each uses a different definition of the addressable market. The honest answer is that Turkey will roughly double in revenue by 2031 under all three published projections, with the spread coming from disagreement on facilitator fees and ancillary spend.

|

Year |

Mordor Intelligence |

Coherent Market Insights |

Future Market Insights |

|---|---|---|---|

|

2026 |

USD 4.59 bn |

USD 4.60 bn |

USD 4.20 bn |

|

2027 |

USD 5.31 bn (est.) |

USD 5.27 bn (est.) |

USD 4.54 bn (est.) |

|

2028 |

USD 6.14 bn (est.) |

USD 6.05 bn (est.) |

USD 4.90 bn (est.) |

|

2029 |

USD 7.10 bn (est.) |

USD 6.94 bn (est.) |

USD 5.29 bn (est.) |

|

2030 |

USD 8.21 bn (est.) |

USD 7.96 bn (est.) |

USD 5.71 bn (est.) |

|

2031 |

USD 9.49 bn |

USD 9.13 bn (est.) |

USD 6.17 bn (est.) |

|

CAGR base |

15.64 % |

14.7 % |

8.0 % |

Mordor and Coherent treat the entire facilitator-and-hospital revenue chain as in-scope, while Future Market Insights uses a narrower hospital-receipts definition. Either way the direction is up. The risk case is regulatory friction outpacing capacity build-out, leaving accredited hospitals at full capacity while licensed facilitators absorb demand at thinner margins.

What These Numbers Mean for Patients

Statistics are useful only if they change a decision. Three patient-level implications follow from the 2026 data.

- Pick accredited, not just cheap. The unlicensed-clinic shake-out is real. Verifying JCI accreditation or HealthTürkiye portal listing is now the most reliable filter, not Instagram presence.

- Budget for the trip, not the procedure. Trip add-ons are 25 to 35 percent of the all-in cost. Treat them as a line item, not an afterthought.

- Ask about complication insurance. The 2025 regulation requires it for licensed facilities. If a clinic cannot show the policy, walk away.

- Plan post-treatment follow-up at home. The CDC Yellow Book 2025 still flags continuity of care as the top medical-tourism risk. Get the discharge summary, lab results, and a contact number for the operating surgeon before you fly back.

Frequently Asked Questions

How big is the Turkey medical tourism market in 2026?

Forecasts cluster around USD 4.2 to 4.6 billion in 2026, with Mordor Intelligence at USD 4.59 billion and Coherent Market Insights at USD 4.60 billion. The official USHAS direct-receipts figure is lower because it excludes facilitator and ancillary spend.

How many international patients does Turkey treat per year?

The most recent USHAS figure is 1,506,442 health visitors in 2024, slightly below the 2023 record of 1,538,643. Q2 2025 alone recorded 733,798 visitors and USD 1.39 billion in revenue, putting 2025 on pace for a similar full-year total.

Which countries send the most patients to Turkey?

Western Europe leads at roughly 32 percent of inbound volume, followed by the GCC and wider Middle East at about 24 percent. Lead source countries are the UK, Germany, Saudi Arabia, the UAE, the Netherlands, and Iraq.

What are the most popular procedures?

Cosmetic and plastic surgery is the largest revenue category at 38.5 percent. Hair transplantation is the most procedurally famous, accounting for over half of specialty-clinic revenue. Dental and bariatric work round out the top four.

How much do patients save by choosing Turkey?

Procedure-only savings range from 50 to 80 percent versus the US and UK, depending on the surgery. Including flights, hotel, and transfers, the all-in saving narrows to 40 to 70 percent, still a large gap but smaller than headline numbers suggest.

How many hospitals in Turkey are JCI-accredited?

42 hospitals in Turkey hold JCI accreditation as of 2025, the second-largest national cluster in the world after the UAE. Ten Turkish facilities also rank at HIMSS Level 6 or higher for digital maturity.

Is the Turkish market still expanding after the 2024 patient dip?

Yes, in revenue terms. Patient volume softened by roughly 32,000 cases between 2023 and 2024, but revenue held flat at USD 3.0 billion. The market is shifting toward fewer, higher-spending cases as unlicensed operators are pushed out by HealthTürkiye portal compliance.

What is the forecast CAGR through 2031?

Published CAGRs for the 2026 to 2031 window range from 8.0 percent (Future Market Insights, narrow definition) to 15.64 percent (Mordor Intelligence, broad definition). Most analysts cluster between 14 and 16 percent.

Data Sources

All figures in this report carry a year and a source. The list below shows where each major number originated. Where two sources gave conflicting numbers, we cited the more recent one and noted the difference in the relevant section.

- USHAS (Uluslararasi Saglik Hizmetleri A.S.), Quarterly health tourism statistics, 2024 and 2025.

- TURKSTAT, Health tourism series 2015 to 2024.

- Mordor Intelligence, Turkey Medical Tourism Market Report, January 2026.

- Coherent Market Insights, Turkey Medical Tourism Market 2025 to 2032.

- Future Market Insights, Turkey Medical Tourism Provincial Outlook 2026 to 2036, January 2026.

- Global Market Insights, Turkey Medical Tourism Market Report 2026 to 2035, March 2026.

- Grand View Research, Medical Tourism Market Industry Report 2025 to 2035.

- Patients Beyond Borders, Global medical tourism patient counts and average spend, 2024.

- Joint Commission International, Accredited organizations directory, 2025.

- OECD Health Statistics, Health expenditure data, 2024.

- Republic of Turkey Ministry of Health, HealthTürkiye portal regulation announcements, May 2025.

- CDC Yellow Book, Medical Tourism chapter, 2025.

- Medical Tourism Association sector reports, 2024 to 2025.

- A-Medical internal facilitator data, 2024 to 2025 caseload (anonymized).

Closing Note

Turkey’s position in 2026 is a study in maturing demand. Headline patient numbers softened slightly while revenue held, accreditation standards tightened, and the procedure mix shifted toward higher-acuity cases. Patients planning a trip in 2026 are choosing from a smaller set of compliant providers but at higher quality and clearer pricing than five years ago. For those considering a Turkish facility, working with a HealthTürkiye-registered facilitator such as A-Medical can simplify portal registration, complication-insurance verification, and post-treatment follow-up coordination from a single point of contact.